For some people, personal finance is second nature. Some were taught by their parents. Others were taught in high school as part of a class called home economics— long before home ec turned into a baking class. For many people, though, understanding how to budget, plan for expenses, manage, leverage and avoid debt is a mystery.

We may learn bits and pieces of finance from advertising. We see ads using buzzy statements to draw you in, such as “Credit Scores Matter!,” “$0 down!,” “No payments until 2018!” But those are ads, not lessons. They’re marketing ploys to get you to do something they want you to do. They are not sound financial advice.

Moreover, because most of our parents struggled with their own personal finances, their financial advice isn’t always helpful. The lesson many of us were taught is that you don’t talk about money.

Even worse, some of us learned you should never ask for help if you have money troubles, as though having debt somehow makes you a bad person. It doesn’t, but payday-loan companies and other high-interest, short-term lenders rely on the fact that you’re more likely to turn to a loan shark than ask your friends or family for financial help.

The high-interest loan industry is built on knowing that your debt-shame will likely keep you stuck in a vicious debt cycle rather than ask for help. It’s time to stop pretending we understand personal finance and actually learn it. Fortunately, the basics are pretty easy to learn.

Over the next few weeks, Ask An Attorney will be talking about the basics of personal finance. If teaching this can help even a few people avoid needing a debt-relief attorney, we’ll be happy that we’ve done our job.

Before we begin, it’s important to remember that even if you have debt, or your financial situation seems hopeless, it isn’t too late. No matter how deep you are, it’s always possible to reset your financial situation back to zero and start fresh.

Ready? Let’s begin.

Step one: Deposit your income in one location

Money comes in and money goes out. Many people have a good idea of how much money they earn after taxes because they get the same paycheck over and over again, at regular intervals. Unless you work in a tip-based industry, figuring out how much you have coming in every month is easy.

If you do work in a tip-based industry, as many Las Vegas residents do, this can be a little harder to figure out, but it’s still doable. What’s the easiest way? Every night when you get tipped out, take it straight to your bank or credit union and deposit it. All of it.

We’ll get to why cash can be bad in a little while, but the easiest way to really track your income is to dump it all into the same piggy bank before you spend a dime.

Step two: Get a bank account if you don’t have one

Don’t have a bank account? Get one.

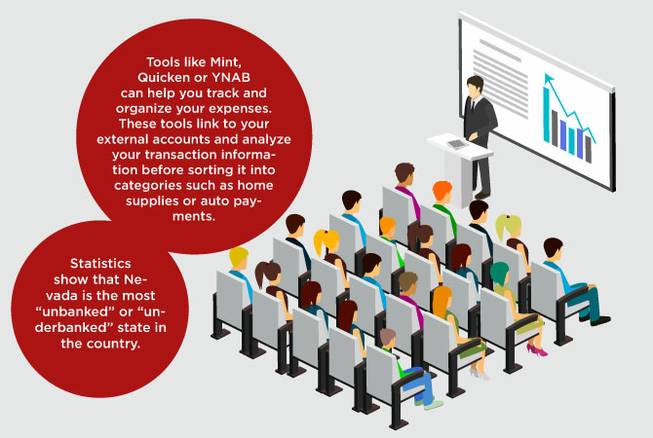

Statistics show that Nevada is the most “unbanked” or “underbanked” state in the country. Recent reports from the Census Bureau and FDIC state that more than 25 percent of Nevadans don’t have a bank account or don’t fully utilize banks for their financial transactions.

We’ll talk more about this in a future article, but with several banks and credit unions having “new start” or “fresh start” banking programs, even people with fresh bruises on recent accounts can get a checking account with a debit card again. There’s truly no legitimate excuse not to have an account anymore.

Why do you need a bank account? It all comes back to tracking your finances, and having a checking account can be a great tool when creating your budget.

Step three: Use a debit card for everything

The most important step in understanding your own personal finances is knowing exactly what your income and expenses are each month. The easiest way to do this is to stop spending cash. You can use your debit card for nearly everything these days, and everything you do with it gets tracked.

$1.07 getting a soda refill at the gas station? Tracked.

$37.29 picking up your dry cleaning weekly? Tracked.

$257.42 in groceries for the family this week? Tracked.

Using a debit card means all of your spending — every penny — is tracked for you. You don’t have to do anything more than you already do; just earn, spend and check your statements.

Some people argue that spending cash versus using plastic makes you more aware of the money you’re spending. You literally feel the dollars leave your hands, but “feeling money” is worthless for tracking purposes. Using a card, you can track every single transaction you make, down to the last cent of your tip at Starbucks, and then categorize those expenses so they’re easy to understand.

Yes, you could track all of your expenses manually, but how many people have the time and patience to do that? We have the 21st century benefit of computers recording our transactions anyway, so let’s take advantage of it.

Once all of your income and expenses are being tracked in one place and you know how much is coming in and how much is going out, the next step is to streamline that information.

Step four: Monitor and analyze your spending

Computers can make this easy. Some banks will categorize everything for you via their online tools, and some people use external tools such as Mint, Quicken or YNAB to categorize their expenses. These tools link to your external accounts and analyze your transaction information before sorting it into categories such as home supplies or auto payments.

You can even create your own categories to better personalize your spending habits and see where your money is going.

The automatic bucketing into categories isn’t perfect, but it’s a good start. When using these tools, you should spend some time every day, or 20 minutes every week, going through the transaction log and making sure your expenses were categorized properly. In the beginning, your categories don’t need to be very detailed.

For example, lumping gas, insurance and a car payment into “auto and transport” is fine for now. You just need to answer the question: How much am I spending on the car?

Tracking, categorizing and understanding your income and expenses are some of the most important things you can do financially. Once you’ve done that, you’re leaps and bounds ahead of most people and well on your way to building your first budget.