When choosing car insurance, many tend to pick the cheapest option that fulfills the minimum legal requirement, but that’s not always enough. Choosing the right insurance policy can be achieved, even on a budget.

If you’re shopping for a new policy or haven’t evaluated your existing policy in a while, the beginning of the year is a good time to do so.

Follow this guide to learn what you’re covered for, what you should be covered for, and where you can cut costs.

Personal liability insurance

There are two types of liability insurance you’re required to have in order to drive legally.

Bodily Injury Liability (BIL): Covers physical harm to people you injure when you’re at fault in a crash. When insurance is listed as a series of numbers, the first two are your policy limits for BIL. “15/30/10” means your insurance will cover injuries to a single person of up to $15,000 or to multiple people up to $30,000 (with no person getting more than $15,000).

Property Damage Liability: Covers repairs to the victim’s property (cars, fences, land, etc.). When you’re shopping for insurance, this number is third after your BIL limits. Using our example above, “10” means your insurance covers up to $10,000 of property damage that you cause, per accident.

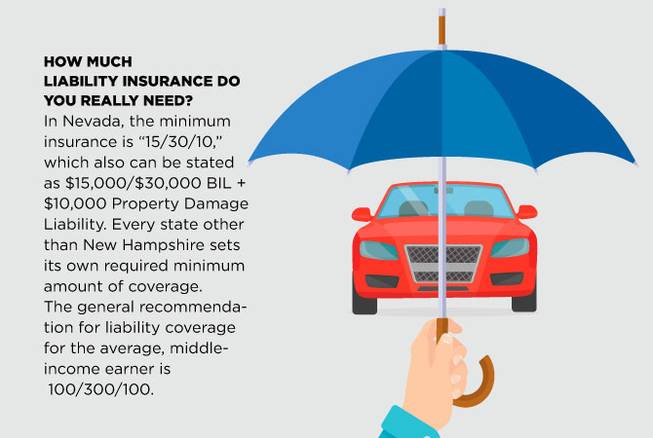

How much liability insurance do you really need?

In Nevada, the minimum insurance is “15/30/10,” which also can be stated as $15,000/$30,000 BIL + $10,000 Property Damage Liability.

Every state other than New Hampshire sets its own required minimum amount of coverage.

The general recommendation for liability coverage for the average, middle-income earner is 100/300/100, with 100/300 of uninsured motorist/underinsured motorist coverage (UM/UIM) to match it (see next page for explanation of UM/UIM).

While this number is high compared with Nevada’s minimum, the cost for a higher insurance level doesn’t increase exponentially. If you’re strapped for cash and/or drive infrequently, 50/100/50 (with 50/100 UM/UIM) should be considered the bare minimum.

According to the National Highway Traffic Safety Administration in 2010, the average “serious” accident resulted in an average of $48,620 in medical bills per injured victim. If you’re only carrying $15,000 of bodily injury insurance, the injured party may sue you for the rest.

Remember, liability insurance does not cover you — your injuries, injuries to your passengers or damages to your vehicle — in any way.

If you opt for a liability plan that only covers 15/30/10, you may be held responsible for any costs beyond the coverage amount.

Additional types of add-on insurance

• Uninsured/underinsured motorist coverage:

This covers injuries to you or your passengers that are caused by an uninsured or underinsured driver, or a hit-and-run driver.

UM/UIM insurance is written like BIL (15/30, 50/100, 100/300, etc.) with two numbers referring to per person/per accident.

Why you need it

According to the Insurance Research Council, 12 to 15 percent of Nevada drivers are uninsured and countless more have only the Nevada minimum 15/30/10 liability insurance, which makes them underinsured in the large majority of circumstances.

Because of this, the odds are high that if you’re hit by a driver in Nevada, he or she will not have enough insurance to cover your medical bills if you’re injured.

For instance, if you’re hit by a driver who only has Nevada’s minimum liability insurance ($15,000) but the collision leaves you with $48,620 in medical bills, your own UM/UIM insurance can cover the remaining $33,620 (if you have enough coverage).

Note: Most insurance companies limit your UM/UIM coverage so that it can’t be more than your Bodily Injury Liability insurance. This is to prevent people from loading up on UM/UIM, which is much cheaper than BIL.

• Collision and comprehensive:

Collision insurance covers damages to your car in the event of an accident, even when you’re at fault. Comprehensive insurance covers losses caused by theft or damages caused by something other than an accident, such as falling objects, fires, windstorms, vandalism, etc.

Some insurance companies combine collision coverage and comprehensive coverage.

Why you should consider it

Collision and/or comprehensive coverage is handy to have in some circumstances, and it’s usually required by the bank if you’re financing your car.

When pricing collision/comprehensive, the higher the deductible, the lower the cost of the insurance. But before you set a sky-high deductible, you need to ask yourself whether you can afford to pay it if something happens.

A $2,500 deductible is great if you never crash, but if you don’t have that kind of money and you get hit, you could find yourself without a car.

• Personal injury protection (PIP, also known as Medical Payments Insurance or MedPay):

Covers the medical expenses and wages lost for you or your passengers, even if you’re the at-fault driver.

Why you should consider it

If you have personal health insurance, PIP/MedPay coverage may not be necessary because your health insurance likely will cover anything that PIP insurance will.

However, if you don’t have health insurance, or if you have high maximum out-of-pocket health insurance, PIP coverage can be invaluable.

If you have a question you’d like to see answered by an attorney in a future issue, please write to questions@PandALawFirm.com or visit PandaLawFirm.com.

Please note: The information in this column is intended for general purposes only and is not to be considered legal or professional advice of any kind. You should seek advice that is specific to your problem before taking or refraining from any action and should not rely on the information in this column.