Student loan debt and the cost of higher education in the United States are hotly contested and pressing issues for consumers, educational institutions and lawmakers. Marketwatch reports there is $1.3 trillion owed in student loan debt in this country, making it the second-largest type of consumer debt behind only mortgages. Further, about 11.6 percent of that debt ($146 billion) is delinquent. With an estimated 40 million Americans owing on student loans, understanding ways to help deal with this debt is important.

It’s also important to note that there are two types of student loans: federal and private. About 10 percent of all student loan debt is private. Understand that while the government programs mentioned here don’t apply to private student loan debt, several lenders have internal programs that mirror government options for forbearance and consolidation.

Government programs to help with federal loans

The government has set up a few programs to help consumers pay off and/or lower their student loan debts when they’re having trouble keeping up with payments. Under limited circumstances, some people may even be eligible for student loan forgiveness.

Here are some options:

• Income-based repayment plan: For people whose income is too low to let them reasonably make their monthly payments, there are four kinds of income-based repayment plans. Under these plans, most people will be able to get their payments down to 10 to 20 percent of their discretionary income.

• Loan consolidation: People with multiple student loans may be able to combine them into one large loan. This can simplify the debt, allowing people to make one single monthly payment, and may even lower that payment.

• Deferment: Under some circumstances, people may be eligible to defer their loans, postponing or reducing monthly payments. Common reasons for deferment include enrolling in college classes, graduate fellowship programs, active military duty, unemployment and financial hardship.

• Student loan forgiveness: It is possible to have student loan debt forgiven. The most common forgiveness program is for teachers, but many government jobs have forgiveness as part of their benefits packages, too. For a list of jobs that may have forgiveness programs attached, see usajobs.gov.

People can learn more about these options and apply for some of them at ed.gov; however, the application process can take months and require lots of confusing paperwork. If you’re applying for one of these programs on your own and need help, you can seek counsel from a debt-relief attorney or, in some cases, the loan service itself.

Avoiding student loan debt

Student loan debt can take decades, even a lifetime, to pay off in full and can cause serious distress for the debtors and their families. People should avoid taking out these loans whenever possible and instead thoroughly investigate scholarships and grants available.

A common misconception is that scholarships and grants are reserved only for geniuses and athletes. That’s not the case.

Every year, tens of millions of dollars in grant and scholarship money go unclaimed, and these are dollars that could be available to anyone. Before taking out any student loans, be sure you’ve found and applied for every scholarship opportunity possible.

Be wary of programs offering to eliminate your debt

Many agencies promise to eradicate your debt, often operating online or over the phone, and claiming to have a “unique” or “proprietary” system for approaching student loan debt. Be leery of companies touting services like this or ones asserting that they’ll be able to do something about your student loan debt that you wouldn’t be able to do on your own.

The truth is, people can do this on their own. Some may feel more comfortable doing so with the assistance of an attorney, but don’t buy into any company making grand claims about being able to fix student loan debt issues.

Can I get rid of my loans through bankruptcy?

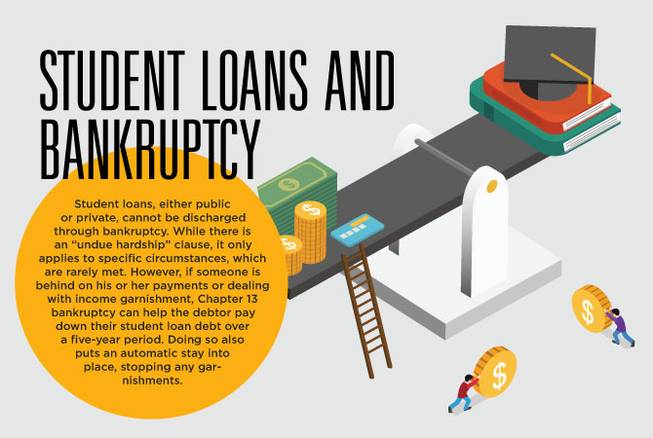

Student loans, either public or private, cannot be discharged through bankruptcy. While there is an “undue hardship” clause, it only applies to specific circumstances, which are rarely met. However, if someone is behind on his or her payments or dealing with income garnishment, Chapter 13 bankruptcy can help the debtor pay down their student loan debt over a five-year period. Doing so also puts an automatic stay into place, stopping any garnishments.

Other things to note…

Be hesitant to take out any student loans to attend a trade school, such as art, culinary or tech schools. The credits received at many of these institutions are nontransferable, and fees paid to attend may not justify the salaries earned upon graduation.

If you take out a student loan, you’ll have to repay it whether or not you actually graduate or find a job. If you’re considering student loans, analyze your job prospects and expected salaries before applying. Racking up $100,000 or more in debt for a job that’s going to earn you $40,000 per year may not make financial sense.